Blockchain in simple terms is a very long and distributed chain of blocks of transaction information. It uses the distributed ledger technology (DLT) which consists of continuously growing (endless) list of transaction records which are called Blocks (blocks of information).

Blockchain first came to existence in 2008, to make it secure the blocks were interlinked with a unique identification include date/time stamps and a trusted party digital signature/stamp. The blocks were also distributed across worldwide large pool of computers to ensure it is impossible to erase or alter any recorded block of information. The conceptual model was then introduced for use for crypto currency bitcoin from year 2009 and since then it served as public DLT for all bitcoin transaction records.

Let’s understand how blockchains work,

1. As Blockchains use the distributed ledger technology (DLT), they are managed using peer-to-peer (P2P) network of computers spread across the world.

2. The computers called as nodes are generally running the digital ledger of transaction records called as blocks.

3. Each node (computer) uses the consensus algorithm protocol for adding and validating new transactions records called as blocks.

4. Every block is distributed across the world involving many computer systems. Each block has the previous blocks unique identification information for validation and integrity of blocks.

5. Blocks hold information of transactions records in an encoded Hash Tree format where each leaf of the hash tree (in this case the block) has the encoded cryptographic hash of pervious block.

6. The information on the blocks is interlinked to each other using this unique cryptographic hash and other relevant information about the transaction, date and time when the block was created and recorded.

7. The blocks once recorded can’t be deleted or altered in any way. They permanently remain on the chain of records and remain retrievable.

8. Blocks can be created but only the longest forming blockchain confirms the reliability of the block. In additions the entire network of computers can validate and confirm if the block and block chain is valid as per their records or not.

9. As each block is replicated across the entire blockchain network of computers and each computer stores all the blocks information, it takes a lot of time for the blocks to be created and validated across the network.

10. As the size of the DLT (distributed ledger network) increases the speed of the block creation and validation reduces. E.g., a block creation for bitcoin having very huge network and extra-large size ledger could take up to 15 minutes while for the new bitcoins it can be done within 30 to 60 seconds as the ledger and size of network is limited.

11. The blockchains can’t be altered so incase of new regulations or rules introduction from a specific date and time, will result in a New Hard Fork creation to identify and use the blockchains under that specific fork.

Now that we understand what blockchains are, let’s move to the types of blockchains. Here are the types of blockchain,

1. Public Blockchain – Public blockchains are open to all decentralized blockchains. All people with internet access can use such blockchains to send their transaction records as well as become the node using consensus protocol to be able to validate records for their authenticity. Such blockchains work based on incentive mechanism where each node gets some incentives for the storage and validations done. E.g., Bitcoin and Ethereum are examples of public blockchain.

2. Private Blockchain – As the name suggests, the private blockchain is restricted access blockchain. The access is strictly restricted for both creator and validator nodes. Such blockchains use distributed ledger technology (DLT) and can called as centralized blockchain to a large extent. E.g., Banking organizations can use Private Blockchain

3. Hybrid Blockchain – A combi of Public and Private can be called as hybrid blockchain were certain areas of the blockchain can be kept public with open access and remaining areas private with restricted access. E.g., Healthcare organizations can use Hybrid Blockchain

4. Consortium or Side Blockchain – These are blockchain where a ledger of blockchain transaction records (blocks) run parallel to primary blockchain. Entries from primary blockchain are linked to the side blockchain. Consortiums and Groups or even group of countries, companies etc. can use this type of blockchain. E.g., Monetary authority can run consortium blockchain with all banks and financial institutions, allowing banks to have their separate side blockchain with links to the primary consortium blockchain.

Here are some pros and cons of blockchain technology,

Pros for Blockchain include,

1. Increased transparency and authenticity – Blockchain verify information across worldwide nodes to ensure transaction is authentic. The ledger in public blockchain is open to all for easy access and full transparency.

2. Permanent Ledger of blocks – Blocks of transactions records never get old or archived. They always remain available in the blockchain across the world. So there is no chance of having any lost transaction records on the blockchain unless all nodes (computers) in the blockchain are altered.

3. Easy Track and Trace – All blocks in the blockchain are always interlinked in such a way that entire chain of blocks remain fully intact. This makes tracking and tracing easier.

4. Cost Savings – This depends on how the blockchain is used. E.g., if blockchain is used for smart contracts of real estate ownerships in a country. It will ensure the entire process is digitalized and contracts are put in blocks with all relevant information making them always available. Savings come from paper, archive stores and people.

Cons for Blockchain include,

1. Implementation Challenges – Blockchain functions using distributed and often decentralized network of nodes spread across the world. It is difficult to trace, monitor and maintain the nodes efficiency and effectiveness. In addition, the adoption and usage itself could be also challenging depending on the area of use.

2. Regulatory Compliance – Blockchain are still not widely accepted technology by major institutions. Although it functions well for crypto currencies and several other trails. For crypto currency itself regulatory compliance issues exist across the world.

3. Technology complexity – Blockchain upgrades, maintenance and support as well as patching and security upgrades for nodes across the world can be very complex to achieve.

4. Future Technology – While blockchain is one of the newest technologies but its adaption has been slow due to unforeseen future of what next and how the entire ecosystem can evolve.

There are many blockchain platforms in use across the world. Here some of the top ones,

1. IBM Blockchain – IBM platform offers a fully managed blockchain-as-a-service solution which can be configured, developed and deployed by organizations for their own use.

2. Ethereum – Ethereum is a decentralized blockchain platform that can be used for smart contracts and in many ways, it operates similar to the bitcoin blockchain platform.

3. Ripple, Tron and Stellar – These are three different blockchain providers but they have similar capabilities as Ethereum.

4. Chainalysis KYT (Know Your Transaction) – KYT blockchain platform is one of the latest and easy to use platforms with latest technology gaining a lot of popularity.

5. Hyper Ledger – Fabric and Sawtooth – These are two different blockchain platforms that offer application creation ability. Sawtooth is an opensource version while fabric is not.

6. Multichain – It is an open source blockchain platform for use by organizations with ability to create both public and private blockchains.

7. Kakao Klaytn Blockchain – It is a blockchain platform by Kakao, its modular network design and architecture makes it easy to use for businesses to configure, customize and operate service-oriented blockchains based on the proprietary Klaytn framework.

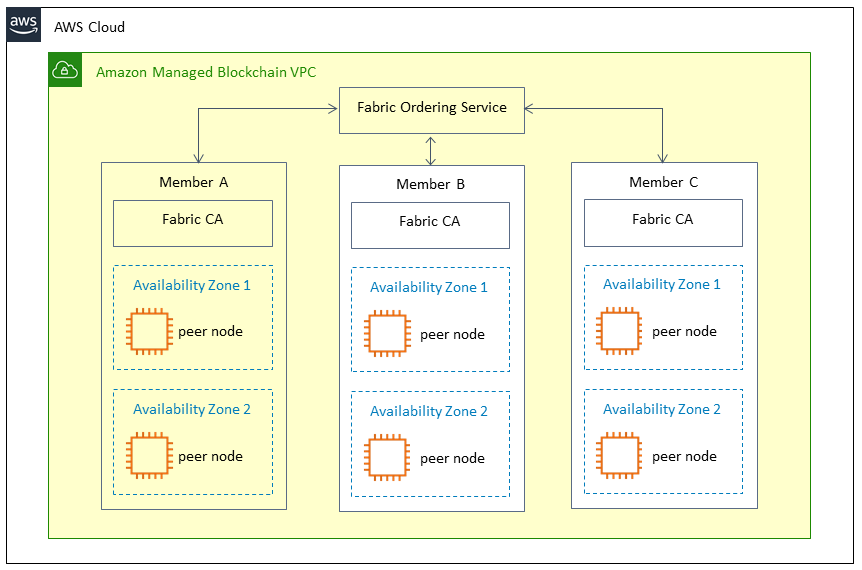

8. Amazon, Azure Quorum and Google Blockchain – The top 3 cloud providers also offer blockchain as a service platform for quick configuration and use by organizations. Here a simple overview of AWS Blockchain architecture as a reference.

Over the years the acceptance and use of various types of bitcoins increased and still continuing to increase. This resulted in financial institutions, monetary authorities and governments to start thinking in the direction of how to control and add good governance model around bitcoins. Many countries are thinking of bringing digital currency (similar to bitcoin) but under governance and control of respective monetary authorities and governments. It is very likely that the underlying technology and ecosystem to be similar or enhanced version of Blockchain making them universally accepted and usable across the world.

For the year 2019 Gartner reported that only 5% of CIOs believed blockchain technology was a ‘game-changer’ for their business as blockchain usage is largely recognized for use only for FinTech organizations, the likes of banks, investment firms, credit card companies and finance divisions.

As we are now in 2022, Blockchain is used in various shapes and forms by almost all the major industries and sectors. Confirmed usage and use cases can be found for Automotive, Banking, Financial services, Government, Healthcare, HealthTech, life sciences, Insurance, Media, Entertainment, Retail, Consumer goods, Logistics and Telecommunications.